Maximum Confidence Long-term Plans Were Considered

Maximum Confidence Long-term Plans Were Considered is a Driver of Elevation Goal 2: Delighting existing clients, promoting advocacy and retention

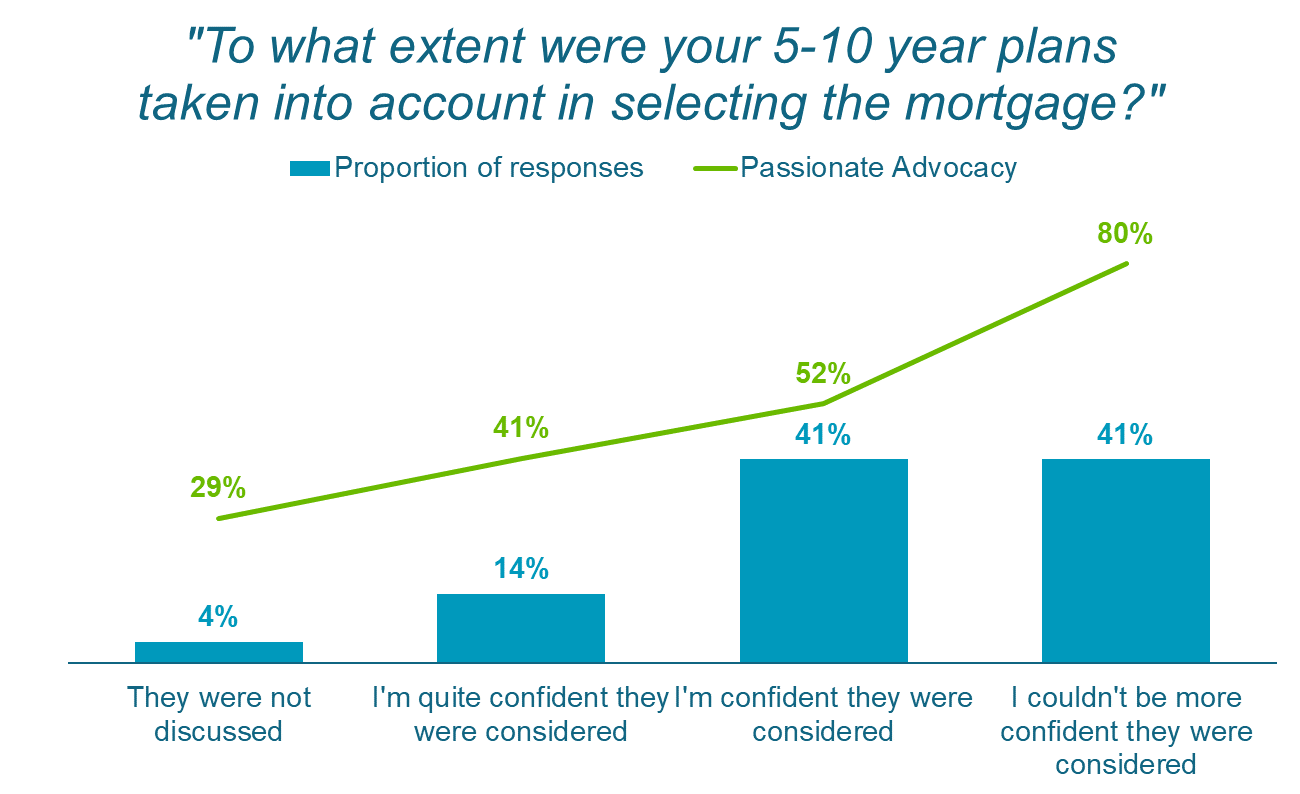

Data based on responses to the following question, asked in the Verified Client review form

"To what extent were your 5-10 year plans taken into account in selecting the mortgage?"

Possible responses

They were not discussed

I'm quite confident they were considered

I'm confident they were considered

I couldn't be more confident they were considered

Maximum Confidence Long-term Plans Were Considered Score

Proportion of respondents answering “I couldn't be more confident they were considered”

Distribution of responses to Maximum Confidence Long-term Plans Were Considered

The relationship between Passionate Advocacy and consideration of long-term plans is highly statistically significant

Why do we ask about Maximum Confidence Long-term Plans Were Considered?

Confidence in the quality of the service arose as a key driver of advocacy from our research with mortgage advice clients. In our conversations with firms, advisers and consumers, we learned that a key way to build that confidence is to ensure that the client knows that any recommendations have been made in the context of their long term plans.

We confirmed this relationship quantitatively through our review forms.

How to improve your score:

Goal-focussed

Choose your language carefully. By exchanging “how can I help?” for “what are you looking to achieve?”, you’re straight into your client’s motivation for sitting in front of you. People are most comfortable when talking about themselves, so your client is likely to be more talkative when discussing what they want to achieve.

Beware starting with money. NEVER start your conversation talking about money. “Do you know what mortgage you want” is an immediate turn off for your client as it suggests you’re not interested in them as individuals. It also keeps the conversation at a superficial level rather than finding your client’s real motivation.

Establish clear goals. It’s important to clearly establish your client’s goals. This is much broader than the mortgage they’ve come to talk about, but what they’re hoping to achieve in life.

Dive deep. Whilst that may sound like an unnecessary level of information, the more you understand about your client, the more you can help. By sourcing the best mortgage, but also making referrals to other services they need, or by helping them to really think about the best route to achieve their goals.

Connect goals to emotion. By focussing on goals rather than products, you’ll create a deeper emotional connection with the client, which will go towards creating passionate advocacy.

Visualise the future

Ask your client what they see in their future. The key is the word see as the aim is to get your client to visualise what they are doing in the future.

Ask guiding questions such as;

- Do you have any (any more) children?

- Where are you living?

- What job are you doing?

By getting your client to visualise their future, it will force them to consider decisions/conversations they’ve been putting off thinking about. These decisions/conversations could impact how their future looks and therefore the best mortgage for them.

WARNING: This can be the point where a couple disagrees or have different visions of the future. It may spark a heated debate, but you’re doing your clients a favour by getting any differences of opinion out into the open. Many couples don’t talk together about the future; however, a mortgage is a long-term commitment, so you need to know what their future looks like to ensure you provide the best mortgage for them.

Validate

Repeat back. Confirm that your client believes that this mortgage fits with their longer-term plans. If they pause, or say no, you know it’s time to revisit their longer-term plans to see what doesn’t fit.

Validate. Ask your client if there is anything they think could happen which would change their longer-term plans. The answer may be no, but it’s good to give them the opportunity to say so. This could also be an excellent introduction to a protection conversation.

Focusing on goals is a sure-fire way to get a longer-term picture of the client’s life. By getting your client to visualise their future, you can establish both their short and longer-term goals and source an appropriate mortgage. Asking your client if they believe the mortgage meets their longer-term goals, validates that they feel confident it does, and gives them the chance to say no if they don’t.